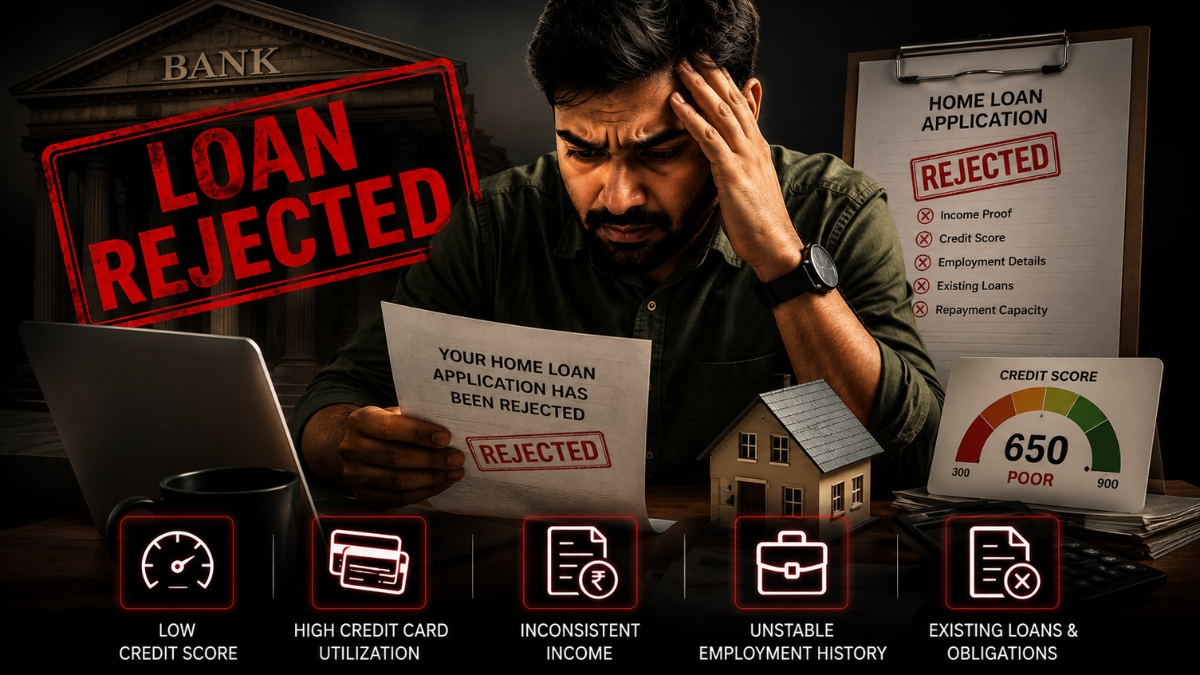

Home Loan Rejected? 5 Hidden Reasons Banks Never Tell You

NEW DELHI, June 8: You booked the flat. You applied for loan. Bank said "No" – with no explanation.

Here is what they hide from you.

1. Your Company is on Their "Negative List"

Startups? Small private firm? Frequent layoffs? Bank has an internal list. If your company is on it – reject.

Fix: Ask HR which banks have tie-ups with your company.

2. Your FOIR is Too High

FOIR = (Existing EMIs + New EMI) ÷ Monthly Income

Above 50%? Reject.

Example: ₹1 lakh salary. Car loan ₹15k. New EMI ₹40k. Total ₹55k = 55% FOIR. Rejected.

Fix: Close small loans first.

3. Property is on "Blacklisted" Location

No OC? Disputed land? Unauthorised colony? Stilt+4 floors? Bank's legal team will reject property.

Fix: Get bank's approved project list before booking.

4. You Took Too Many Small Loans Recently

2-3 personal loans or credit cards in last 6 months? Bank thinks you are "credit hungry".

Fix: Stop taking new loans for 6-12 months before home loan.

5. Unexplained Cash Deposits in Your Account

Cash deposits that don't match your income? Bank assumes tax issue or borrowed down payment.

Fix: Keep bank statement clean. Use proper banking channels.

What To Do Now?

| Step | Action |

|---|---|

| 1 | Ask bank for written reason |

| 2 | Check CIBIL for errors |

| 3 | Apply to a different bank |

| 4 | Wait 3 months – don't apply everywhere |

The Bottom Line

Loan pre-approval before booking flat = safe.

Booking first, then loan = risky.

Share this with someone whose loan got rejected. You might help them fix it.